After Approval: The Quiet Work of Ongoing KYP Monitoring

The most dangerous moment in a KYP process may be the moment everyone feels finished.

The most dangerous moment in a KYP process may be the moment everyone feels finished.

The product has been reviewed. The committee has approved it. Advisors have the materials. Clients have bought it. The file looks complete.

Then time passes.

A fee changes. A risk rating moves. A manager leaves. Liquidity becomes less theoretical. Performance starts behaving differently than expected. The product has not failed, but it is no longer exactly the product that was first reviewed.

That is when KYP becomes real.

Monitoring is not the same as noticing

Most firms notice things.

An alert comes in. A wholesaler sends an update. A fund company releases a notice. A product appears on a watchlist. Someone forwards an email.

Noticing is useful. It is not enough.

Monitoring means the firm has a way to decide whether a change matters, who should review it, what action is required, and whether affected clients need a suitability reassessment.

Without that next step, information piles up without becoming judgment.

The process does not need to be elaborate for every product. It does need to be clear enough that people are not improvising whenever something changes.

Significant change should not be a mystery

A strong monitoring process defines the kinds of changes that may require review.

That definition will vary by product. A major liquidity change may matter more for an illiquid alternative strategy. A manager departure may matter more for an active, concentrated mandate. A risk-rating increase may require a different response depending on how widely the product is held and by whom.

The point is not to create a perfect list.

The point is to avoid making every meaningful change feel like a new debate from scratch.

A useful monitoring process has three parts:

- Triggers: what kinds of product changes require attention?

- Ownership: who reviews the change and decides what it means?

- Evidence: where is the decision recorded?

That may sound basic. In practice, basic is often what saves time.

The firms that struggle are not always careless. They are often unclear. The change is noticed, but no one can say exactly what the next step is.

The hold decision deserves respect

Ongoing monitoring is not only about whether to buy more or sell.

Sometimes the recommendation is to hold.

That can be perfectly reasonable. It can also be poorly documented.

If a product’s risk rating increases and clients continue to hold it, the advisor may need to support why that remains suitable. The answer may differ by client. One client may have modest exposure, high risk capacity, and a long time horizon. Another may have liquidity needs, concentration issues, or a risk profile that no longer fits the product.

The same product change can lead to different client outcomes.

That is why a hold decision after a significant change should not be treated as doing nothing. It is still a decision. The file should show the reasoning.

“Continue to hold” can be a sound recommendation.

It just needs to be more than a shrug.

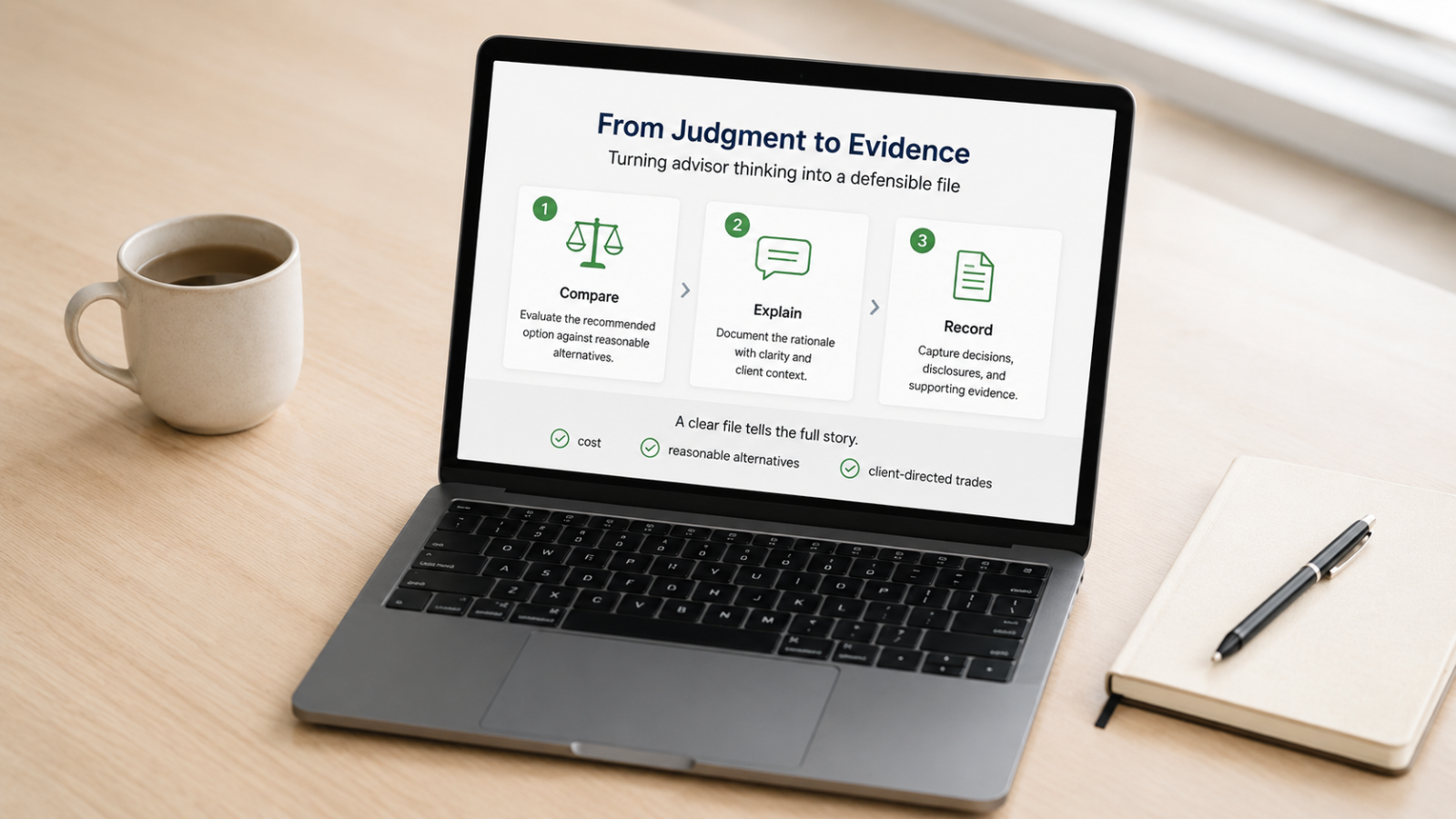

Transfer-ins and client-directed trades are not side doors

Two situations often create friction in real advisor workflows: transferred-in securities and client-directed trades.

They feel different because the advisor did not necessarily initiate the position. The security arrived from another firm, or the client asked for the trade.

But those situations do not remove the need for professional judgment.

A transferred-in security still needs to be understood within a reasonable time. A client-directed trade still requires a suitability determination. If the trade is unsuitable, the advisor needs to explain the concern, recommend a suitable alternative, and document the client’s choice if they proceed anyway.

This is not about blocking clients from making decisions.

It is about making sure the advisor does not become an order taker when the rules require more.

The best systems reduce noise

Good monitoring should not bury advisors in alerts.

Advisors do not need more noise. They need better sorting.

A useful monitoring workflow helps separate the trivial from the meaningful. It identifies the products that changed, the clients who may be affected, and the next action required. It also keeps a record of the decision.

That is the difference between a monitoring process and a notification pile.

Technology can help, but only when it serves the workflow. A watchlist is useful if it leads to review. An alert is useful if it prompts a decision. A dashboard is useful if it makes the next step clearer.

Otherwise, it is just a nicer-looking inbox.

Ongoing KYP is an operating discipline

No advisor can control how every product behaves after it is purchased.

But advisors and firms can control whether meaningful changes are noticed, assessed, connected to client circumstances, and documented.

That is the discipline.

It is not glamorous. It is not a one-time project. It is the quiet work that prevents KYP from becoming a stale file.

Konsyra is built to help with that operating problem: structured product research, watchlist-style monitoring, and documentation support that helps advisors keep track of what changed and why it matters.

Next: monitoring only works if the client side of the equation is strong enough. That takes us to KYC, risk profile, liquidity, and concentration.

Sources

Continue reading

The Documentation Gap: Cost, Alternatives and the Evidence Problem

The file usually fails on proof, not intention.

When KYC Breaks Suitability

Suitability problems often look like product problems. Sometimes they are. But often the weakness began earlier, in the client file.

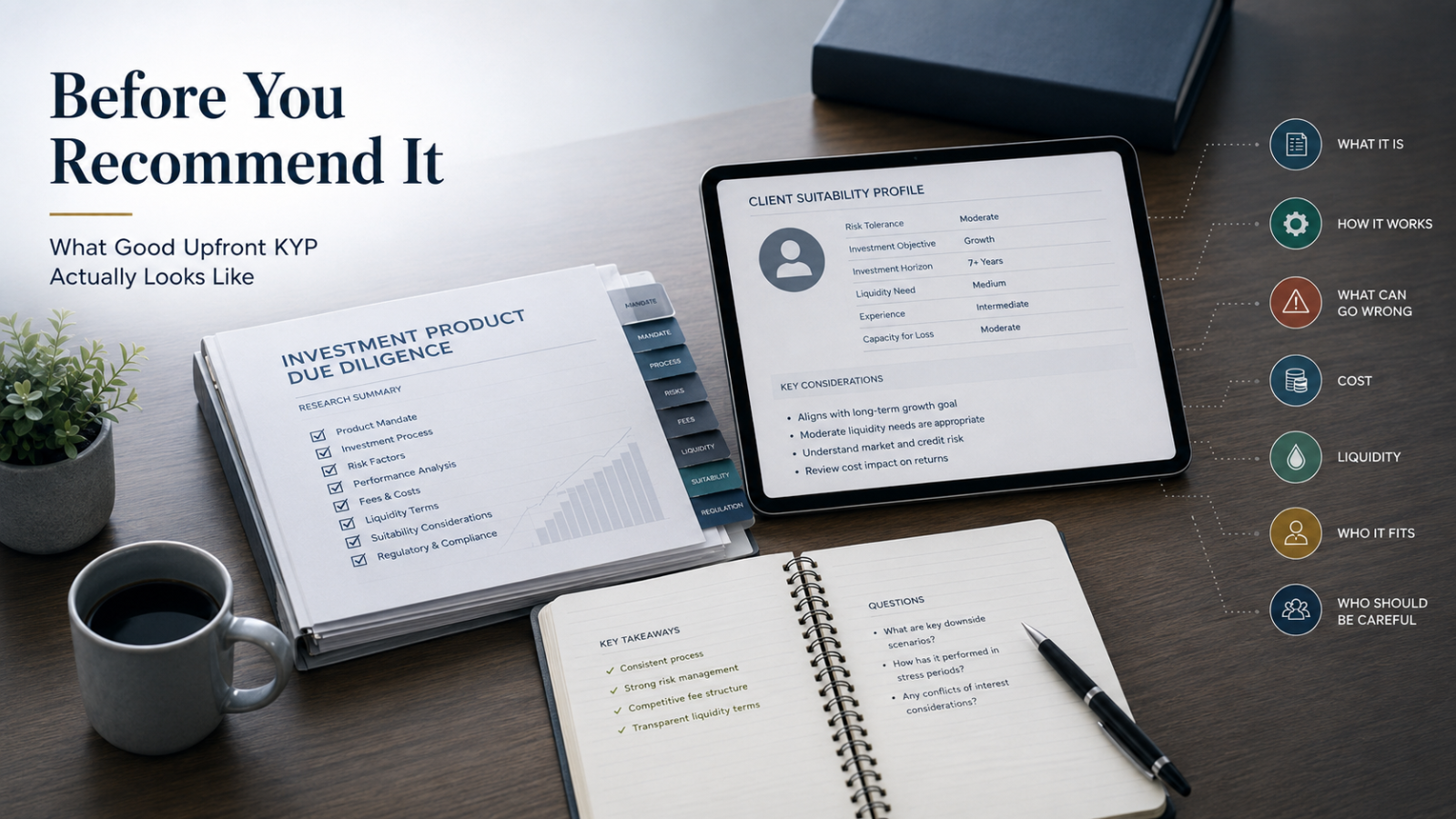

Before You Recommend It: What Good Upfront KYP Actually Looks Like

A product can be approved and still be misunderstood.