Before You Recommend It: What Good Upfront KYP Actually Looks Like

A product can be approved and still be misunderstood.

A product can be approved and still be misunderstood.

That is the uncomfortable truth sitting underneath a lot of KYP work. The approved list tells an advisor that a product made it through the firm’s process. It does not prove the advisor understands how the product behaves, where it fits, what it costs, or when it could become a poor match for a client.

Approval matters.

But approval is not comprehension.

The shelf answers one question

Firm-level KYP asks whether a product should be made available through the firm. The firm looks at structure, features, risks, costs, complexity, liquidity, conflicts, and the type of client the product is intended to serve.

That review is important. It creates the product gate.

But once the product is available, the advisor still has work to do.

The advisor’s question is more specific: do I understand this product well enough to recommend it to this client, in this account, at this time?

That distinction is where a lot of confusion begins.

A broad-market ETF, a mutual fund, a private real estate limited partnership, a structured note, and a model portfolio may all be approved products. They should not all be treated the same way.

The more complex, illiquid, costly, concentrated, or unusual the product, the more explicit the advisor’s understanding should be.

That is not bureaucracy. That is proportionality.

A useful upfront review is practical

A good KYP review does not need to sound like it was written for a tribunal.

It needs to be useful.

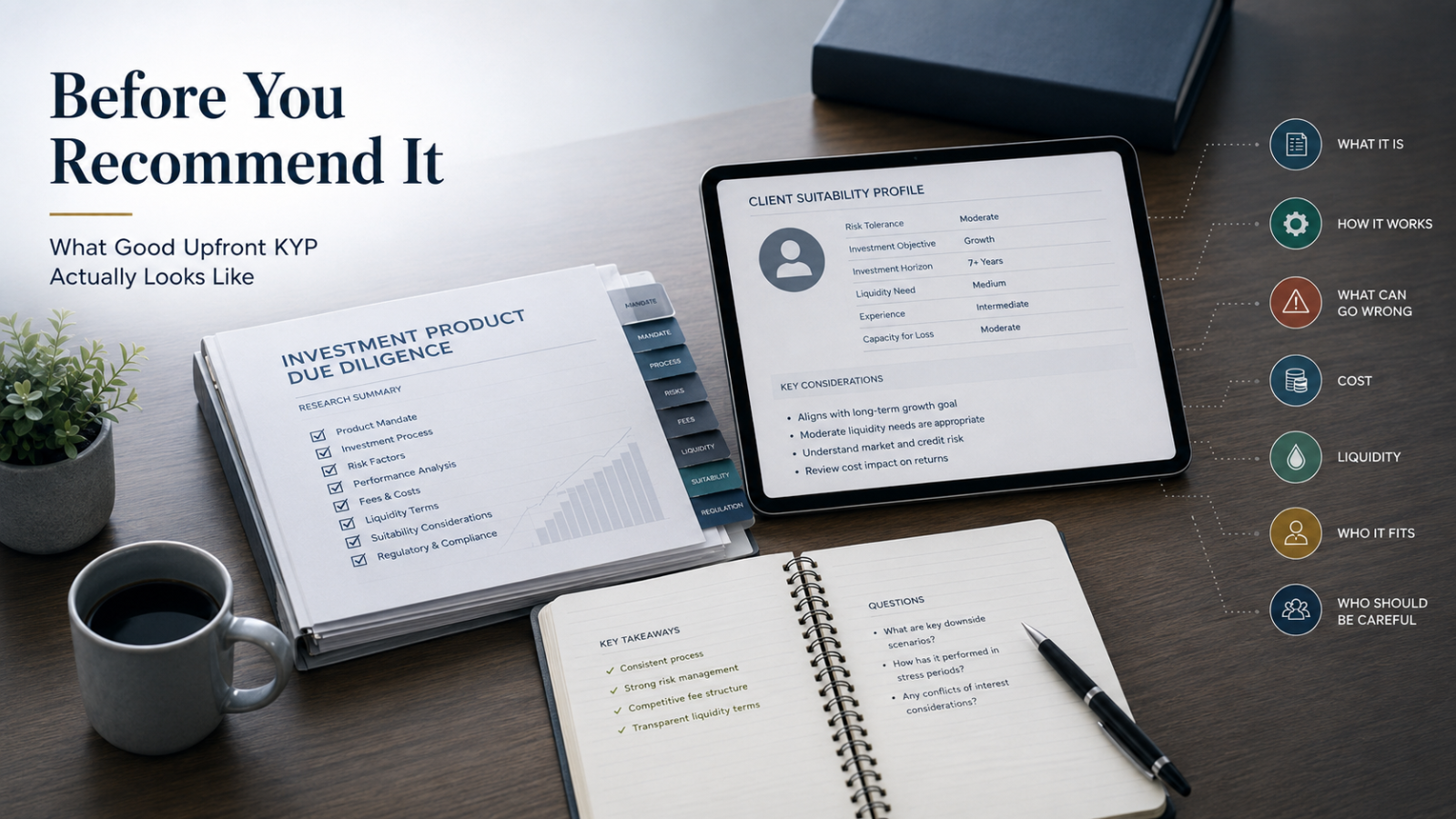

For most advisors, useful means the review helps explain:

- what the product is

- how it works

- what can go wrong

- what it costs

- how liquid it is

- who it may fit

- who it may not fit

The last point is often the most valuable.

Product materials usually spend plenty of time describing the ideal buyer. Good KYP also forces the opposite question. Who should be careful with this?

A product with limited liquidity may be reasonable for a client with long time horizons and excess capital. The same product may be a poor fit for a client who needs flexibility or has uncertain cash needs. A concentrated strategy may be appropriate for a client with high risk capacity and modest exposure. It may be difficult to defend for a client whose risk profile was built on a vague “medium” label and little supporting detail.

The product did not change.

The client did.

That is why KYP cannot be separated from KYC for very long.

Model portfolios still need judgment

Model portfolios can make KYP feel cleaner than it really is.

The allocation is already built. The securities have been selected. The model has a label. The advisor chooses the one that appears to match the client.

That can be efficient. It can also create false comfort.

A model portfolio is still a recommendation. The advisor should understand the model’s composition, risk, cost, intended client type, and how it may behave under stress. If the advisor is permitted to substitute securities or deviate from the model, the need for documentation becomes even more important.

Labels help organize the shelf. They do not replace judgment.

A “balanced” model can mean different things across firms. It can also feel very different to a retired client in a difficult market than it looked in a one-page summary.

The advisor does not need to turn every model recommendation into a thesis. But the records should show enough to explain why that model fit that client.

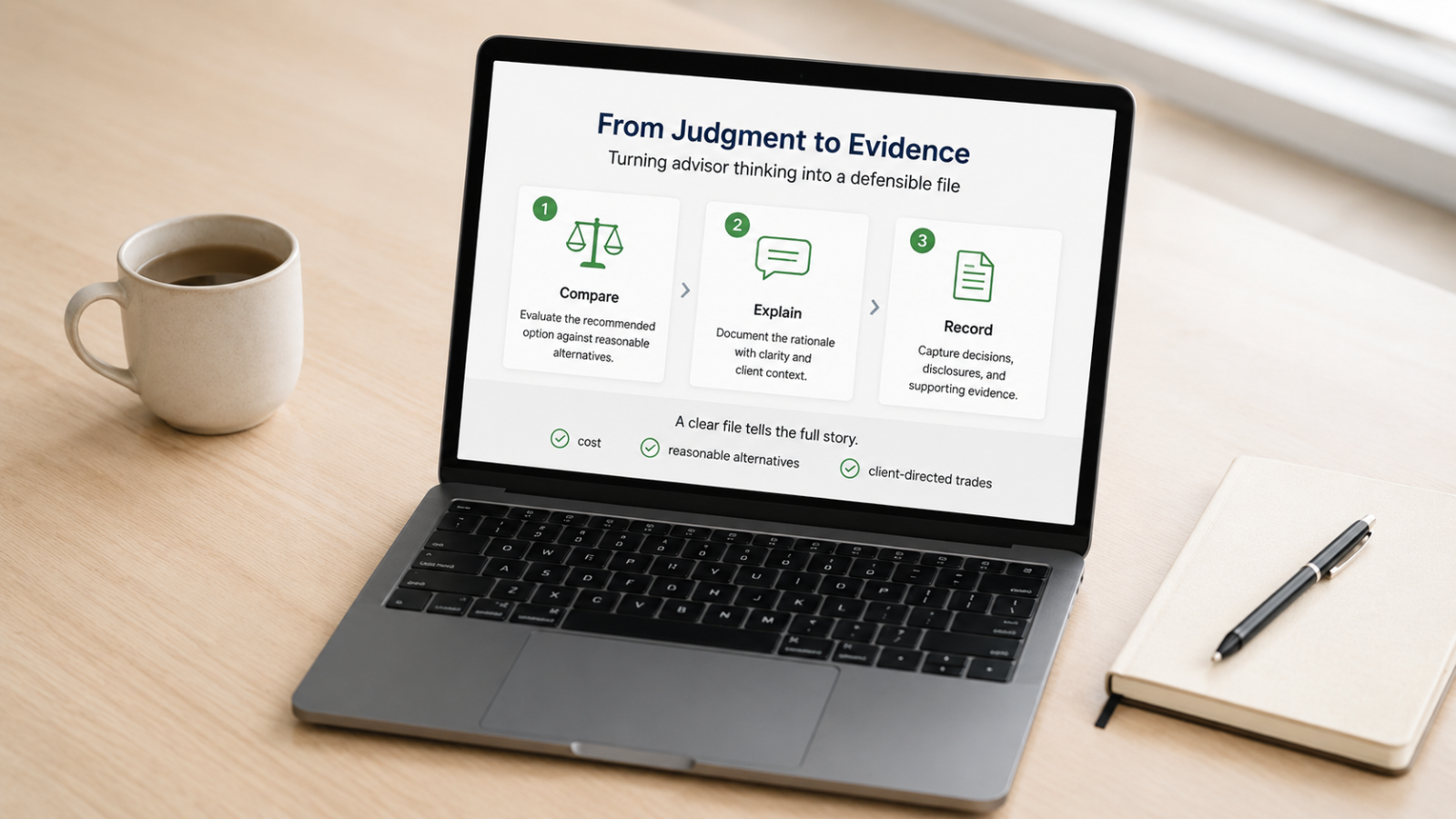

The evidence should match the product

One useful rule: the file should get more detailed as the product gets harder to explain.

A plain, low-cost, liquid product may require a lighter touch. A private, illiquid, higher-fee product should not.

That seems obvious, but it is often where real-world processes break down. Firms may have done work but cannot show it clearly. Advisors may have reviewed materials but left no evidence. Committees may have approved a product but the rationale is hard to find. The review may exist, but it lives in a generic document folder or email inbox.

A defensible process should show who reviewed the product, what mattered, why it was approved, what risks were identified, and what ongoing monitoring is expected.

At the advisor level, the documentation should show enough product understanding to support the recommendation.

Not everything needs a long note. But complexity should leave footprints.

The front end saves time later

Weak upfront KYP rarely stays contained.

It comes back later as supervisory questions, client confusion, re-papering, monitoring gaps, and awkward attempts to reconstruct why something was recommended in the first place.

A cleaner upfront process avoids some of that.

It gives advisors a usable product summary. It clarifies the client types. It flags risks early. It makes costs easier to explain. It creates a starting point for monitoring.

Most importantly, it reduces the chance that the advisor has to rebuild the original logic months or years later.

That is one of the problems Konsyra is built around: helping advisors structure product research and KYP documentation while maintaining an organized, historical record for each .

Next: once a product is approved and recommended, the work is not over. Ongoing monitoring is where KYP either becomes a real process or a file from last year.

Sources

Continue reading

The Documentation Gap: Cost, Alternatives and the Evidence Problem

The file usually fails on proof, not intention.

When KYC Breaks Suitability

Suitability problems often look like product problems. Sometimes they are. But often the weakness began earlier, in the client file.

After Approval: The Quiet Work of Ongoing KYP Monitoring

The most dangerous moment in a KYP process may be the moment everyone feels finished.