When KYC Breaks Suitability

Suitability problems often look like product problems. Sometimes they are. But often the weakness began earlier, in the client file.

Suitability problems often look like product problems.

Sometimes they are. But often the weakness began earlier, in the client file.

The product research may be fine. The recommendation may even be reasonable. But if the client information is vague, stale, or incomplete, the suitability conclusion rests on a weak foundation.

A strong product case cannot fully rescue a poor client record.

The foundation matters most when the recommendation is harder

KYC can feel administrative because it often arrives as forms, fields, and update reminders.

That understates its importance.

KYC is the advisor’s working understanding of the client: personal circumstances, financial circumstances, investment needs, objectives, investment knowledge, risk profile, and time horizon.

The greater the complexity of the recommendation, the more that understanding matters.

A liquid, diversified, low-cost product may not put much pressure on the file. A concentrated, illiquid, higher-fee, or higher-risk product will. The same is true when the client has multiple accounts, external holdings, borrowing, income needs, or changing life circumstances.

Good KYC does not require perfect knowledge of the client’s entire life.

It requires enough information to make the recommendation supportable.

Risk tolerance is only half the story

One of the most practical changes under the Client Focused Reforms is the emphasis on risk profile, not just risk tolerance.

Risk tolerance is what a client is willing to accept.

Risk capacity is what a client can actually withstand.

Those are not always the same.

A client may say they are comfortable with risk because they want higher returns. That does not mean they have the financial ability to absorb loss. A retired client drawing income from the portfolio may have a very different risk capacity than a younger client still saving aggressively, even if both describe themselves as “medium” risk investors.

This is where vague labels create trouble.

Low, medium, and high may be useful shortcuts, but they are not a full analysis. If the client’s stated tolerance conflicts with their financial circumstances, time horizon, liquidity needs, or age, the file should show how the advisor resolved the inconsistency.

Most people are more risk tolerant in theory than in a bad market.

That is not cynicism. It is experience.

Liquidity is boring until it is not

Liquidity rarely feels urgent at the time of purchase.

It becomes urgent when the client needs money.

That is why liquidity needs belong near the centre of the KYC process. An illiquid investment may be entirely appropriate for one client and a poor fit for another. The difference may come down to cash flow, time horizon, outside assets, debt, retirement status, or the client’s need for flexibility.

A product with redemption limits, lockups, valuation uncertainty, or limited secondary market options should put more pressure on the client record.

If the client can afford to wait, that may be fine.

If no one asked, that is a problem.

Concentration does not care how many accounts the client has

Clients experience risk across their financial life, not by account number.

That sounds obvious, but many systems still make it hard to see the full picture. A client may own the same issuer, sector, strategy, asset class, or product type across multiple accounts. They may also hold relevant exposure outside the firm.

No advisor can know everything.

But where concentration risk is likely to matter, the process should help the advisor see enough to make a reasonable judgment.

This is especially important for narrow shelves, illiquid products, sector-specific strategies, exempt market exposure, or recommendations that could meaningfully increase exposure to one issuer or theme.

A concentration issue missed across accounts is still a concentration issue.

The client will not be comforted by the fact that the exposure was neatly divided across statements.

Stale KYC creates hidden risk

KYC does not expire all at once.

It becomes stale quietly.

A client retires. A job is lost. A marriage ends. A business is sold. New debt is taken on. A parent requires support. A client starts drawing more from the portfolio. None of these changes may look like a product issue at first.

But each can change the suitability analysis.

The risk is that the advisor knows something has changed, but the file does not. That gap can be dangerous. The advisor’s actual knowledge has moved ahead of the official record.

When facts change, the file should change too.

That is not paperwork for its own sake. It is how the suitability conclusion stays connected to reality.

Better KYC makes KYP more useful

Product research only becomes useful when applied to real client circumstances.

That is the link between KYC and KYP. The product side tells the advisor what the investment is and how it can behave. The client side tells the advisor whether that behaviour fits.

When KYC is weak, KYP has nowhere solid to land.

Konsyra focuses on the product research, monitoring, and documentation side of the workflow. But the broader lesson is simple: the best advisor processes connect product facts and client facts before the recommendation is made and again when something changes.

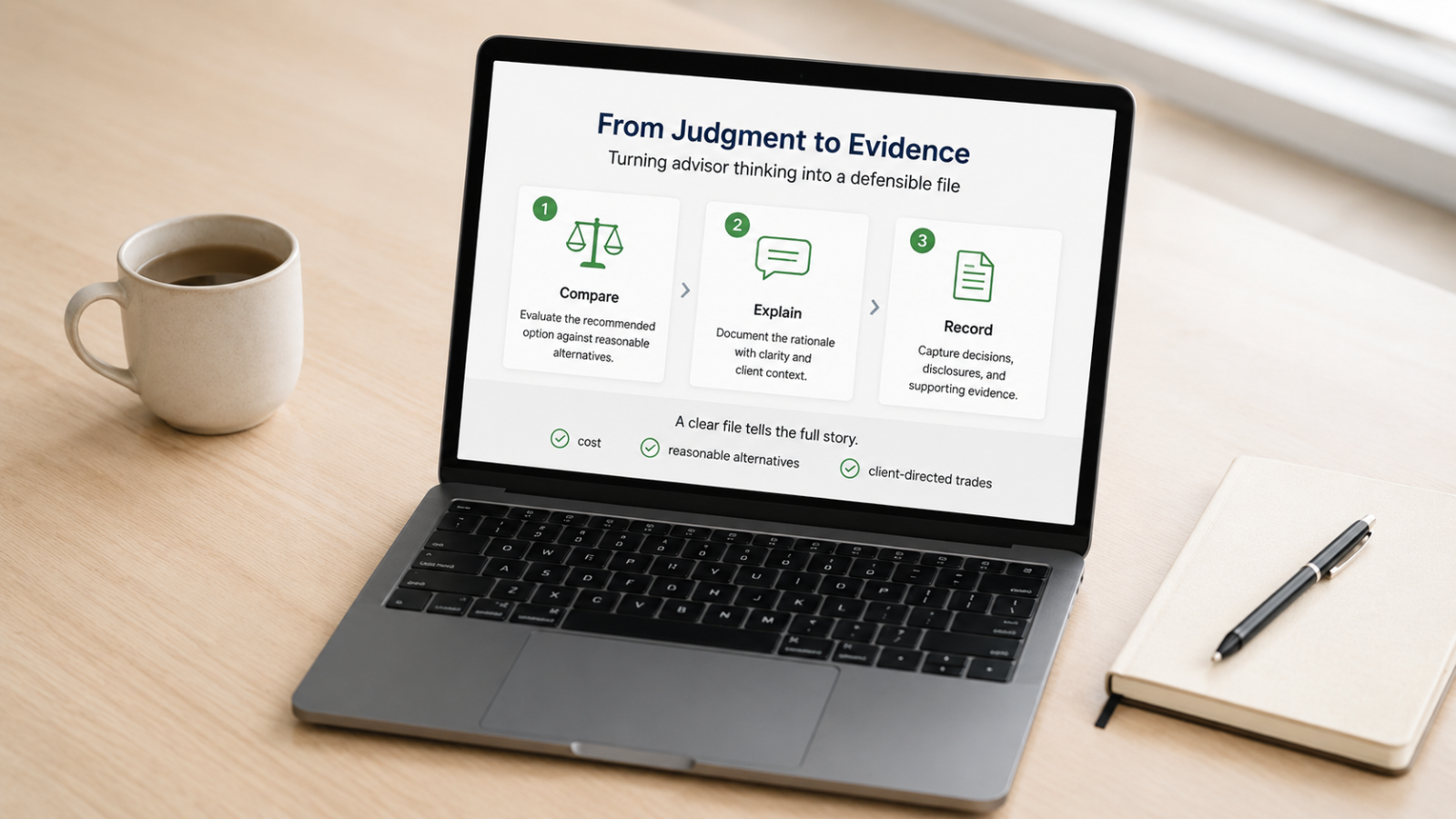

Next: once the product and client are understood, the remaining challenge is evidence. Costs, alternatives, client-directed trades, and documentation are where many files become thinner than the actual thinking behind them.

Sources

Continue reading

The Documentation Gap: Cost, Alternatives and the Evidence Problem

The file usually fails on proof, not intention.

After Approval: The Quiet Work of Ongoing KYP Monitoring

The most dangerous moment in a KYP process may be the moment everyone feels finished.

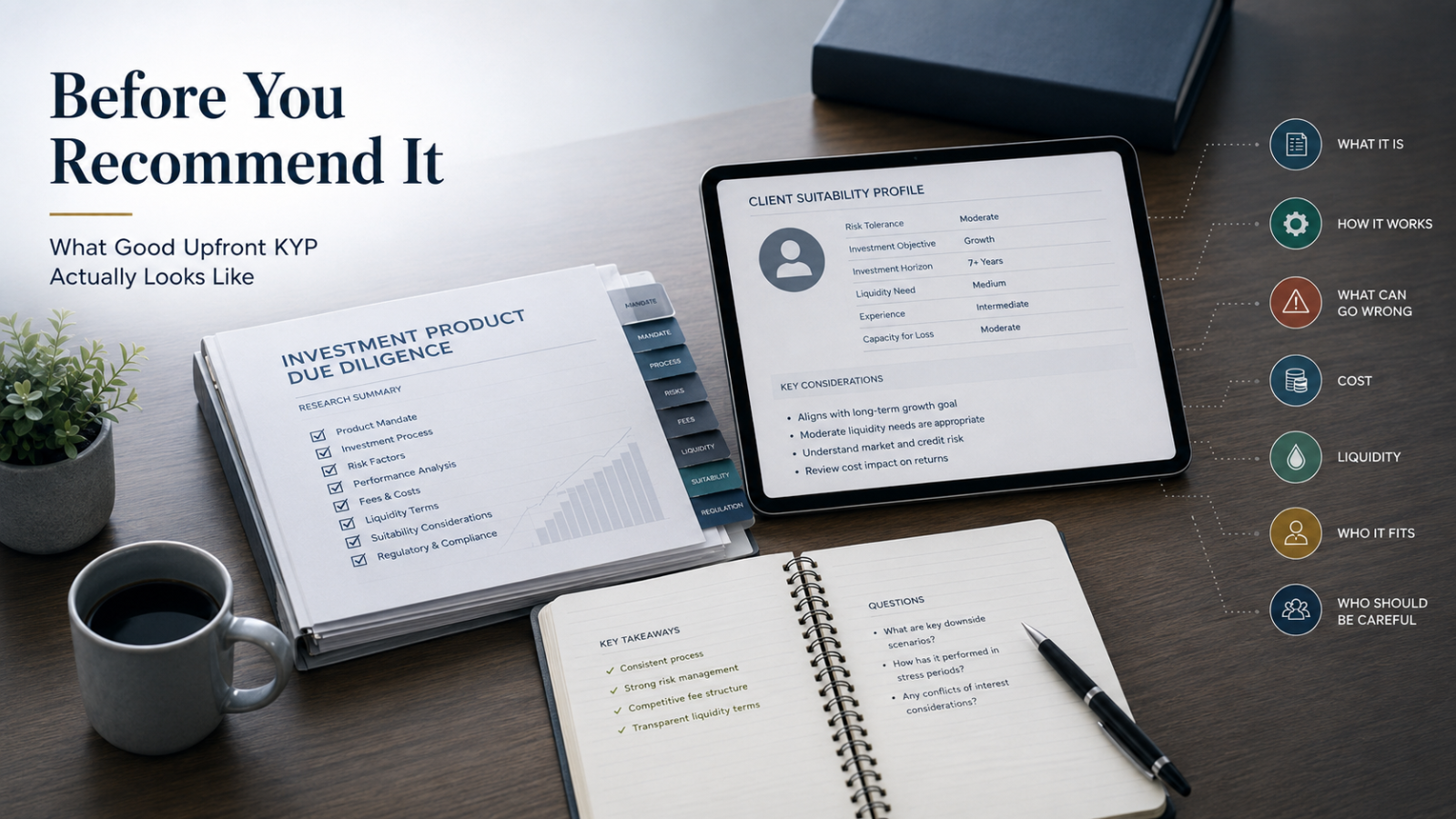

Before You Recommend It: What Good Upfront KYP Actually Looks Like

A product can be approved and still be misunderstood.