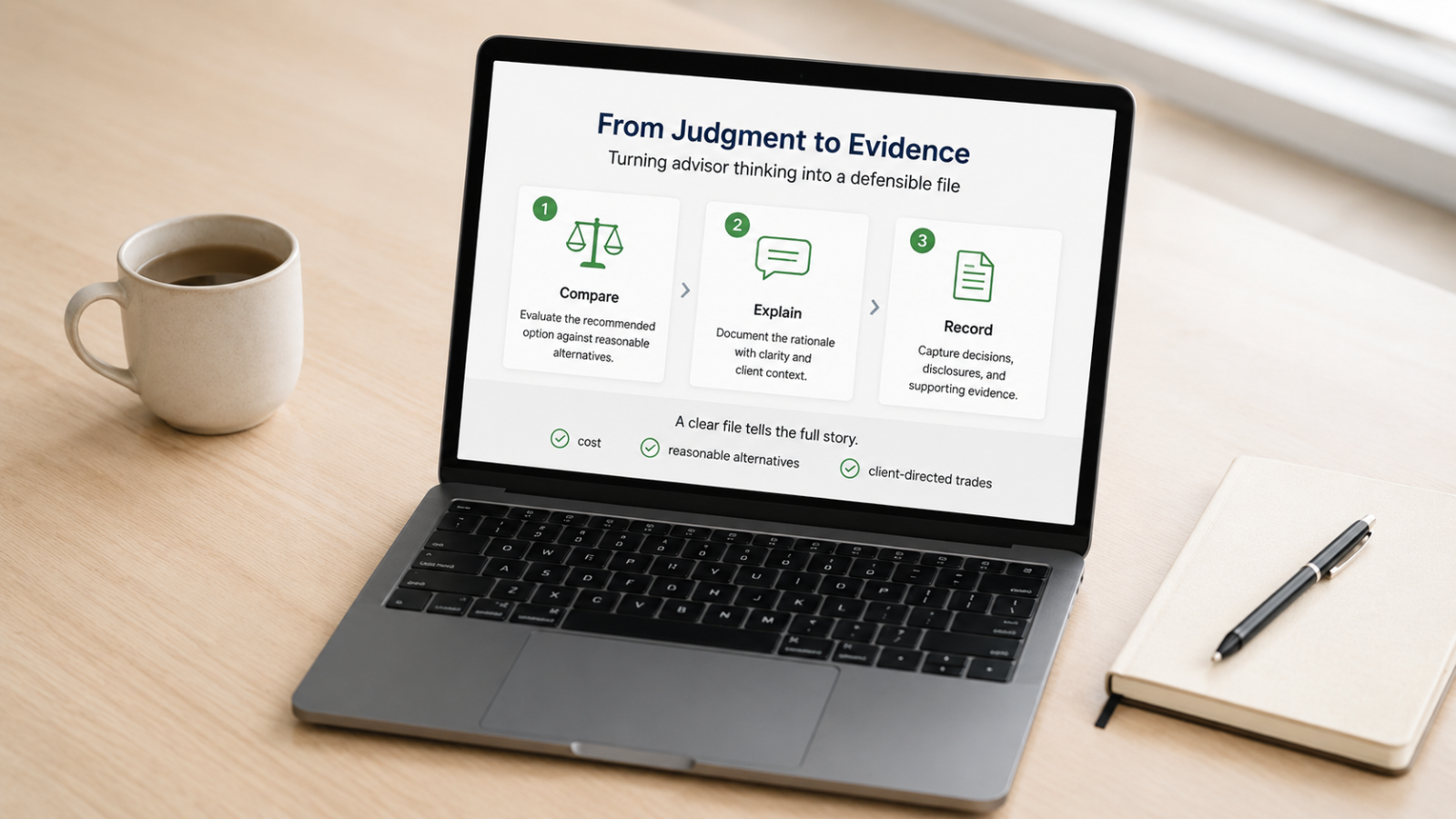

The Documentation Gap: Cost, Alternatives and the Evidence Problem

The file usually fails on proof, not intention.

The file usually fails on proof, not intention.

That is the awkward lesson from many suitability reviews. Advisors may know the client. They may understand the product. They may compare options. They may make a reasonable recommendation.

Then the file tells a thinner story.

The product research is somewhere else. The cost comparison was informal. The KYC update is incomplete. The reason for choosing one option over another lives mostly in the advisor’s head.

That is the documentation gap.

Not bad judgment. Weak evidence.

Cost deserves more than a passing glance

Cost is not the only factor in suitability. It should not be treated as the only thing that matters.

But it does matter.

A higher-cost product is not automatically unsuitable. A lower-cost product is not automatically better. Advice is not a race to the cheapest possible option.

Still, where similar options are available through the firm, the file should show that cost was considered. If a higher-cost option is recommended, there should be a reason.

Maybe the product has a feature that matters. Maybe the lower-cost version is not available to the client. Maybe the higher-cost option fits the service model, tax situation, mandate, structure, or account type better.

Fine.

But the file should not leave everyone guessing.

This is especially relevant where multiple series of the same fund exist, clients become eligible for lower-cost series after reaching asset thresholds, or similar products are available at different cost levels.

Small cost differences can look administrative.

Over time, they can become hard to explain.

Reasonable alternatives are not infinite alternatives

The phrase “reasonable range of alternatives” can sound impossible.

It is not.

It does not mean every advisor must compare every product in the market before every recommendation. It means the firm needs a process that fits its shelf, business model, client base, and investment approach.

A broad-shelf investment dealer may need tools that help advisors compare similar products by cost, risk, liquidity, performance characteristics, and client fit.

A model portfolio platform may handle part of the analysis at the mandate level, with client-level suitability focused on selecting the appropriate model.

A narrow shelf may need to be clear about what alternatives are actually available and how those limits are addressed.

The key is not perfection.

The key is that the process should be explainable.

If no one can describe when alternatives are considered, who considers them, what information is used, and when more documentation is required, then the process may be more assumed than real.

Assumed processes tend to look weak under review.

Client-directed trades still need a professional response

Client-directed trades can be uncomfortable because the client is leading the action.

The client asks to buy the security. The advisor may not have recommended it. Everyone wants to respect the client’s decision and move on.

But client direction does not make suitability disappear.

If the trade is unsuitable, the advisor needs to say so, explain why, recommend a suitable alternative, and document the client’s decision if they proceed anyway.

That is not about being paternalistic.

It is about not confusing client choice with advisor silence.

The distinction matters most when the trade conflicts with the client’s KYC information, creates concentration, introduces liquidity risk, adds meaningful cost, or involves a product the client may not fully understand.

“The client wanted it” may be true.

It may not be enough.

Policies are not workflows

A policy that says advisors must consider costs and alternatives is a start.

It is not a workflow.

A real workflow tells people what to do. It explains what information should be reviewed, what tools should be used, what notes are expected, what requires escalation, and how the answer should be documented.

This is where many firms struggle. The policy restates the rule. The procedure does not explain the day-to-day behaviour.

That gap matters because advisors are busy. If the process is not clear, each advisor is left to invent their own approach.

Some will do it well. Some will not. Most will be inconsistent.

Consistency is not the enemy of judgment. It is what helps good judgment show up in the file.

Short notes beat long reconstructions

Advisors often resist documentation because it feels like extra work.

Fair enough.

But the alternative is often worse: trying to reconstruct the thinking months later.

A useful note does not need to be long. It needs to explain the tradeoff.

Why was this product chosen over the available alternatives? Why did the cost make sense? Why was the concentration acceptable? Why was the product suitable despite any apparent tension with the client’s profile? Why was holding still reasonable after a change?

The file does not need to pretend there were no tradeoffs.

It needs to show that the tradeoffs were considered.

That is the difference between documentation as paperwork and documentation as evidence.

The operating problem

Across this series, the pattern is clear.

KYP is not one task. It is a workflow.

Upfront review. Advisor understanding. Ongoing monitoring. KYC updates. Suitability determinations. Cost analysis. Alternatives. Client-directed trades. Documentation.

Handled poorly, it becomes scattered work. Handled well, it becomes a repeatable process.

The firms that do this well will not necessarily write the longest notes. They will make it easier for advisors to show their thinking consistently without turning every recommendation into an administrative marathon.

That is the problem Konsyra is built to help with: structured KYP research, monitoring support, and documentation workflows that help advisors stay organized while preserving professional judgment.

If you are just joining the series, start with the first article: KYP in the Real World for Canadian Advisors. It lays out the full framework. If this all sounds painfully familiar, it may be worth asking whether your current KYP process is doing enough of the work for you.

Sources

Continue reading

When KYC Breaks Suitability

Suitability problems often look like product problems. Sometimes they are. But often the weakness began earlier, in the client file.

After Approval: The Quiet Work of Ongoing KYP Monitoring

The most dangerous moment in a KYP process may be the moment everyone feels finished.

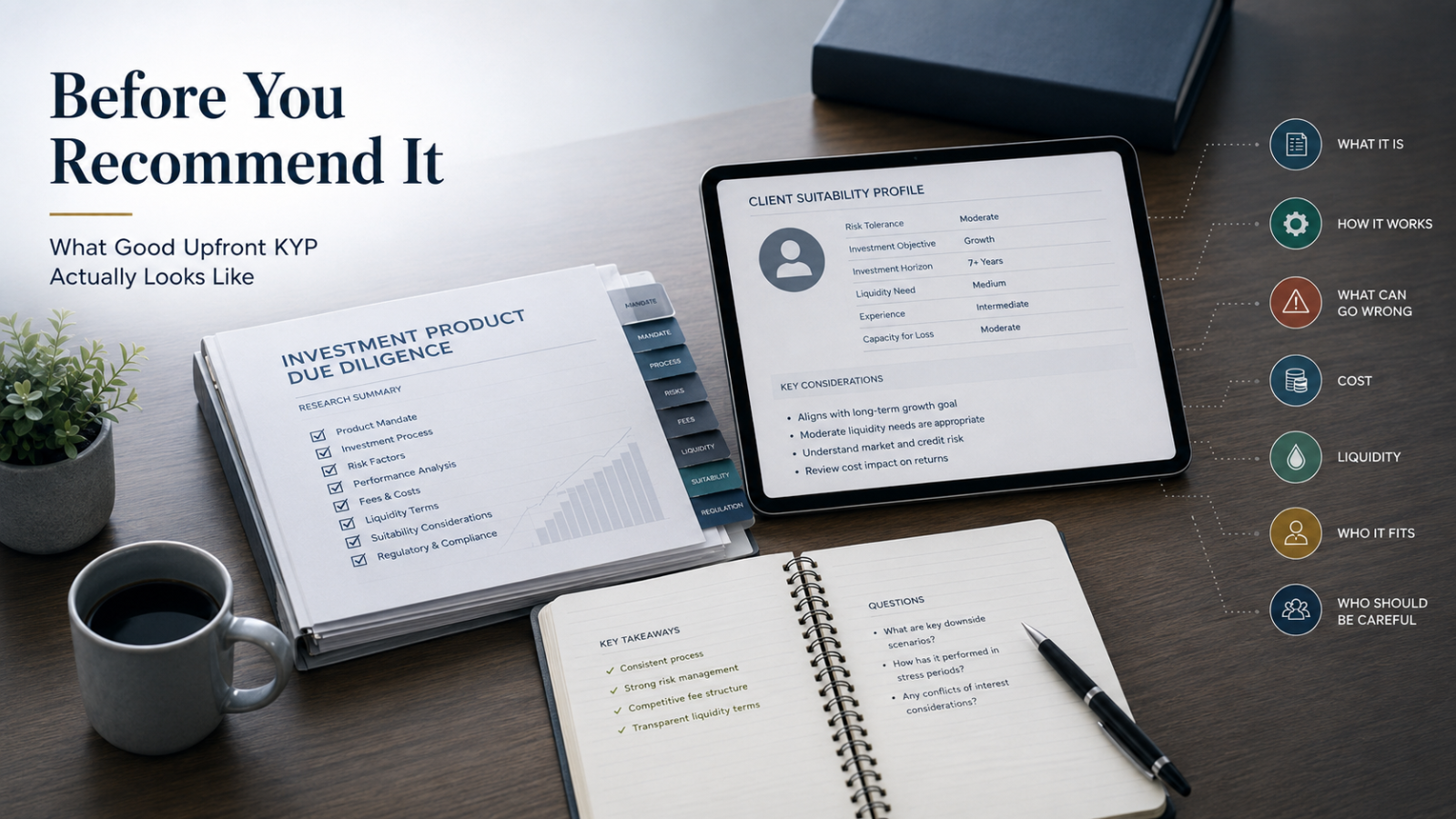

Before You Recommend It: What Good Upfront KYP Actually Looks Like

A product can be approved and still be misunderstood.