KYP in the Real World for Canadian Advisors

Regulators have a funny habit of taking obvious ideas and turning them into paperwork problems.

Regulators have a funny habit of taking obvious ideas and turning them into paperwork problems.

Every advisor already knows they should understand a product before recommending it. That part is not controversial. The harder question is what that sentence means on a Wednesday afternoon, while managing a large book, with back-to-back client meetings, a model portfolio update, an approved list, a new fund series, and a product that looked plain vanilla six months ago but now feels a little less vanilla.

That is where KYP lives now.

Not in the slogan. In the proof.

KYP is no longer just a shelf decision

For a long time, many advisors thought about product due diligence as something that happened somewhere else.

Head office reviewed the product. The product committee approved it. The fund made the shelf. The approved list was updated. The advisor could then focus on the client.

That was never the whole story, but it was an easy story to believe.

The problem is that KYP now has two jobs. The firm has to assess, approve, and monitor the products it makes available. The advisor still has to understand the product well enough to use it with a real client in a real account.

Those are related jobs, but they are not interchangeable.

A firm-level review may explain why a product belongs on the shelf. It does not automatically explain why it belongs in Mrs. Patel’s RRIF, a younger client’s margin account, or a model portfolio built for moderate-risk retirees who care more about liquidity than yield.

That is the practical shift. KYP is not just about whether a product can be sold. It is about whether the advisor can connect the product to the client, the account, the alternatives, the costs, and the facts at the time.

That last phrase matters: at the time.

A file that looks obvious today can look thin two years later if no one can tell what the advisor knew, what changed, or why the recommendation made sense.

The triangle: KYP, KYC, suitability

KYP does not work by itself.

It sits in a triangle with KYC and suitability. If one corner is weak, the whole thing leans.

KYP asks whether the product is understood.

KYC asks whether the client is understood.

Suitability asks whether the investment action makes sense when those two things are put together.

That sounds simple. It is not always simple in practice.

A product can be reasonable. A client can be reasonable. The combination can still be wrong.

A higher-yielding product may be understandable and approved, but not appropriate for a client with near-term liquidity needs. A concentrated position may be fine for one client and dangerous for another. A model portfolio may be suitable for a broad mandate but still require care when assigned to a specific client.

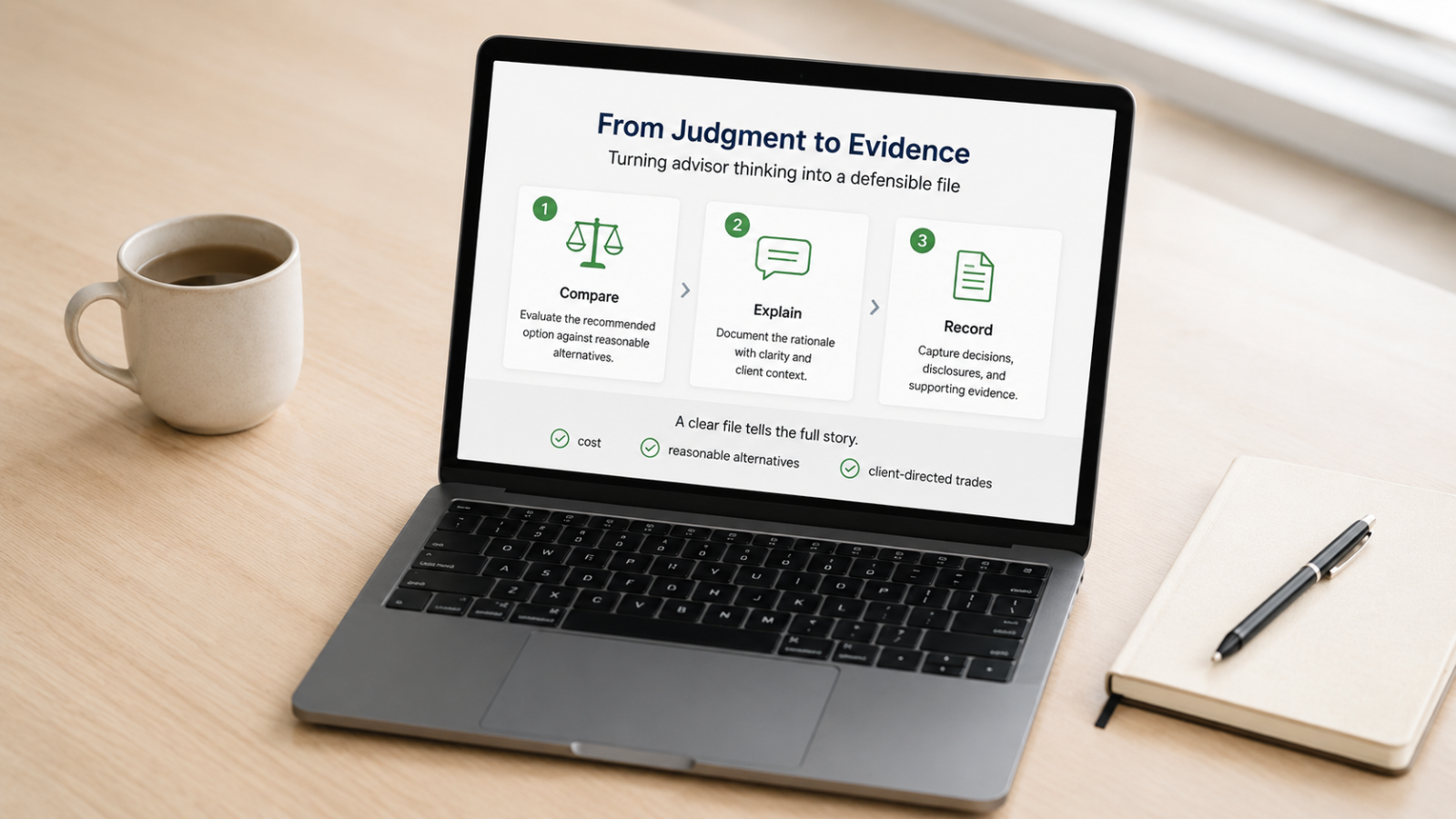

This is why recent regulatory findings have focused so much on evidence. Regulators are not only asking whether advisors meant well. They are asking whether firms and advisors can show how they connected the dots.

Good compliance is often less dramatic than people think. It is not usually about writing a novel. It is about leaving enough trail that a reasonable person can understand the decision later.

Approval is the start, not the finish

One of the easiest traps in KYP is treating approval as the end of the process.

It feels like the finish line because a lot of work happens before a product is approved. Research is gathered. Committees meet. Risks are assessed. Materials are prepared. Someone signs off.

But products do not sit still.

Fees change. Risk ratings move. Liquidity gets tested. Management teams change. Sector exposure becomes more concentrated than expected. A product that behaved one way in calm markets behaves differently when money starts moving quickly.

And sometimes the product did not come from the firm’s shelf at all. It arrived through a transfer-in. Or the client asked to buy it. Those cases can feel like exceptions.

They are not exceptions. CIRO and the CSA are explicit about this.

A client-directed trade still requires a suitability determination. A transfer-in still needs to be understood within a reasonable time. A hold decision after a significant change is still a decision.

That last point is easy to underestimate. Doing nothing can feel like not making a recommendation. But if the product has changed, the client has changed, or the portfolio impact has changed, then “continue to hold” may need just as much support as “buy.”

Silence is not a great file note.

The time burden is real

None of this is free.

Advisors already operate inside a crowded workflow. Client meetings, portfolio reviews, planning, administration, compliance requests, account paperwork, market updates, and the occasional urgent email that arrives five minutes before the next meeting.

KYP adds another layer because it asks for both judgment and evidence.

That is the frustrating part. Most advisors are not trying to avoid the work. They are trying to fit the work into a day that already has too many moving parts.

A good KYP process should not turn every recommendation into a legal memo. It should make the core thinking easier to repeat: what the product is, what can go wrong, who it fits, what changed, and why the recommendation makes sense for this client.

The goal is not more paper for the sake of paper. The goal is a cleaner way to show judgment.

The opportunity for advisors

There is a tempting way to look at KYP as just another compliance burden.

That is understandable. It is also incomplete.

Good KYP can make advisors better at the job. It forces clearer thinking about product fit, client constraints, concentration, liquidity, cost, and alternatives. It can prevent lazy portfolio construction. It can reduce the odds of holding yesterday’s recommendation long after the facts have changed.

It also protects the advisor from one of the most common problems in this business: being right in substance but weak on evidence.

That is a bad place to be. You did the thinking, but the file does not show it.

The best processes solve for that without slowing the advisor down more than necessary.

That is the practical lane Konsyra is focused on: helping advisors structure product research, maintain useful KYP documentation, and monitor investments for changes that may matter. Not replacing advisor judgment. Not making suitability decisions. Just making the research and evidence side of the work easier to manage.

Next: before the monitoring, documentation, and suitability questions, there is the first test. What does good upfront KYP actually look like before a product is recommended?

Sources

Continue reading

The Documentation Gap: Cost, Alternatives and the Evidence Problem

The file usually fails on proof, not intention.

When KYC Breaks Suitability

Suitability problems often look like product problems. Sometimes they are. But often the weakness began earlier, in the client file.

After Approval: The Quiet Work of Ongoing KYP Monitoring

The most dangerous moment in a KYP process may be the moment everyone feels finished.